Canada Can Learn From the UK’s Pay by Bank Experiment

Canada is approaching a critical moment in the development of its open banking framework. Much of the discussion so far has focused on regulation, accreditation, and technical standards. Those elements matter, but experience from more mature markets suggests another factor may be just as important: consumer language.

If Canada wants meaningful adoption of open banking services, it must pay attention not only to infrastructure but to how those services are described to the public.

The United Kingdom provides a useful early lesson. Despite being one of the world’s most advanced open banking markets, consumer understanding of the terminology behind it remains surprisingly low. Open banking payments continue to grow rapidly, yet research suggests many consumers do not recognize the terms used to describe them.

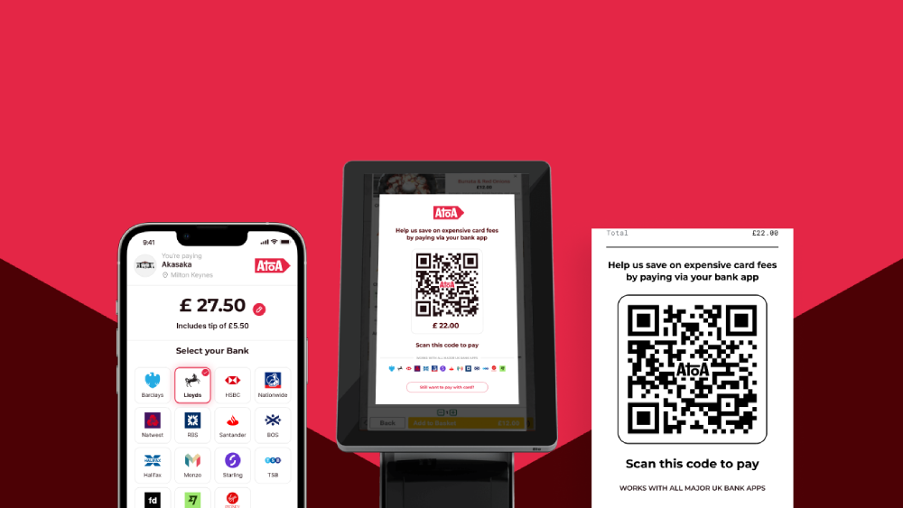

Atoa, a UK payments company helping reduce card fees for businesses.

One example is the phrase “Pay by Bank”, which emerged in the UK as an attempt to give consumers a simple description of what an open banking payment actually does. Instead of entering card details, the consumer authorizes a payment directly from their bank account. The experience is faster and often cheaper for merchants, while reducing fraud risks.

However, recent UK research highlights a growing challenge. Consumer recognition of the term “Pay by Bank” has fallen from 55 percent to 38 percent in the past year. At the same time, the same payment method is often labelled differently depending on where a consumer encounters it. Some merchants call it “open banking payment”. Others use “instant bank transfer” or “account-to-account payment”.

When one experience is described in several different ways, recognition fragments. Consumers struggle to connect the dots, and familiarity never compounds.

The consequence is behavioural. When people do not recognize a payment option, they tend to default to the methods they already trust. In the UK, for example, older payment terminology such as “BACS” remains more widely recognized simply because it has been used consistently for decades.

I am based in the UK and recently I was explaining what I do for work to a friend. Like many people outside financial services, she had never heard the term “open banking”. The phrase meant nothing to her.

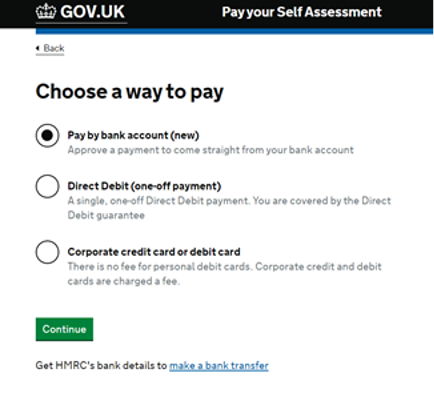

The HMRC’s Pay your Self Assessment payment options screenshot

But when I asked whether she had ever paid her taxes online through HM Revenue & Customs (HMRC), the UK’s tax authority, using the option that allows you to authorize payments directly from your bank account, she immediately recognized it. She had used it several times.

HMRC was in fact one of the earliest large-scale real-world deployments of open banking payment initiation. In 2021 it became the first tax authority in the world to integrate open banking payments into its online services. Within ten months of launch more than one million tax payments had already been made using the service, worth over £3 billion.

Whilst my friend did not know that she had used open banking, she used it nonetheless.

This raises an interesting question for the industry. Does the consumer actually need to know what open banking is?

Consumers rarely care about the infrastructure behind financial services. Most people do not understand how card networks work, what Faster Payments are, or how contactless transactions move between banks. What matters to them is the experience. Is it secure? Is it simple? Does it work without friction?

“Pay by Bank” was designed to communicate exactly that. It focuses on the action. The consumer is paying using their bank account. The underlying rails, APIs, and security frameworks remain invisible.

For Canada, the lesson is not that this specific term must be adopted. The lesson is that terminology matters, and it must be consistent across the ecosystem.

Banks, fintechs, merchants, and government services all play a role in shaping how new payment experiences are presented to consumers. If each actor uses different language to describe the same capability, recognition will remain fragmented and adoption will slow as consumer default back to familiar methods.

Canada has an advantage in that its open banking ecosystem is still forming. That creates an opportunity to align early around clear, consumer-friendly language before multiple competing terms emerge.

Because ultimately, consumers do not adopt infrastructure. They adopt experiences.

If the experience is clear and familiar, the technology behind it will scale naturally.

We welcome conversations with financial institutions, fintechs, and ecosystem partners who are thinking about the role they want to play in this next phase. The direction of Canada’s open data ecosystem will not be shaped by regulation alone, but by the organizations that participate in building the services, partnerships, and use cases that bring it to life.